A disaster of the stock market in 1987 is the Black Monday that left a cut as one of the steepest and unforgettable financial events in the history of the modern era. On October 19, 1987, each of the world’s financial markets demonstrated the highest fall that was followed by the Dow Jones Industrial Average’s collapse of 508 points, thus marking the record for the biggest loss (equivalent to a 22.6% change in one day of trading).

This huge decrease caused a stock market panic that swept the globe and caused widespread panic among investors, institutions, and governments around the world. The factor that made Black Monday so unforgettable was not only the size of the loss, but also the very abruptness with which it had occurred. In the absence of a clear economic reason, the crisis not only revealed the weaknesses of the modern trading infrastructure but also, in particular, computerized program trading.

Such a crisis hastened the basic questions of whether automated systems were capable of losing control of the situation in the blink of an eye or not. Thus, during the subsequent years, regulators and market participants raced against time to develop safety measures to keep a similar financial crash from happening again. This article aims to guide readers through the driving forces behind the unfolding of and the staying power of Black Monday by shedding light on the events and their unfolding, as well as the lessons learned.

The Calm Before the Crash

When Black Monday happened, the US stock market had been on a continuous winning streak for about five years. The period of 1982-1987 showed the DJIA and its value going threefold higher. One of the main reasons was that people bought stock,,s and the price of each share on the stock exchange had suddenly risen. The investors were excited about the gains in the company profits, plus the general attitude was decidedly optimistic. Unsurprisingly, late that year, an indicator had emerged that contradicted such untamed enthusiasm. The increase in the rates of interest was the first of the signs. The US dollar sank significantly against other currencies following the currency agreements, and the market looked like it was at its peak.

Yet, with all of this happening around them, only a few guessed what was in store. In the week prior to October 19, the U.S. stock markets had already become quite shaky showing almost a 10% decrease that was without a doubt the result of the growing panic. Nevertheless, a majority of the investors were optimistic that the market was simply taking a temporary downturn. It was a correction, but not the one that anyone was thinking of.

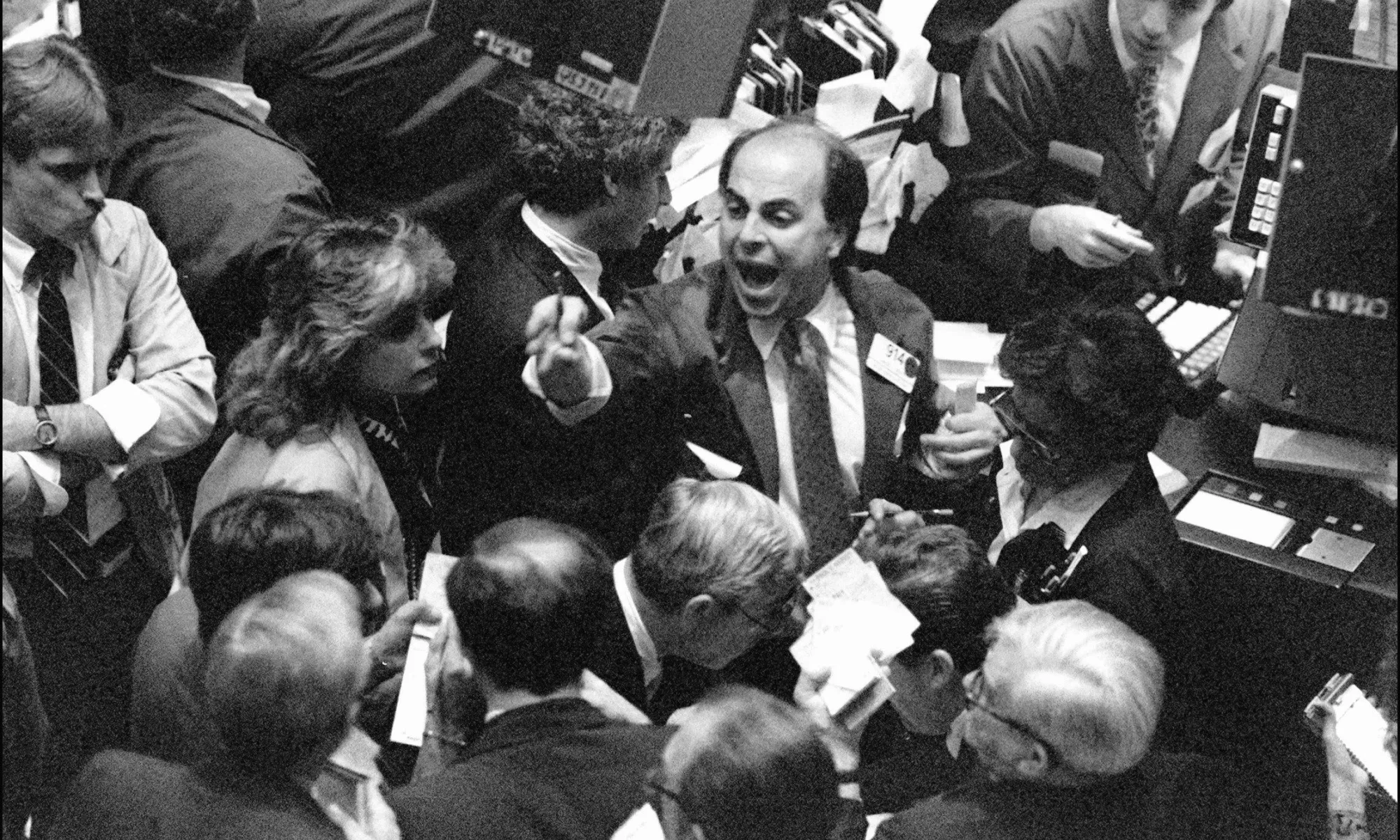

The Anatomy of a Crash: October 19, 1987

Once the trading pit was opened on Monday, panic seized the market almost instantly. A deluge of sell orders came in from every part of the world because hedging and insurance were not there. Automated systems awaiting orders caused the crisis to get out of control. These programs, when there was a drop in the market to certain levels, carried out huge selling orders, and thus, things accelerated faster. As the algorithms went on with the selling, and there were no buy orders to match the selling ones, the result was that the situation collapsed completely.

When the market closed, the DJIA recorded a loss of 22.6% in the value of the stocks. The figure is enormous, as in those days it was the greatest daily index loss in the history of Wall Street, even the days of the 1929 Great Depression. At the same time, the S&P 500 Index crumbled by 20.4%, and stock markets as far as London and Tokyo also went down in price.

It was at this critical point that the phrase “stock market 1987 Black Monday” was coined, and it has become the turning point of that financial year ever since.

The Role of Program Trading and Portfolio Insurance

Portfolio insurance was among the instruments that exacerbated the crisis. Portfolio insurance was a computerized strategy launched in the late 1970s to save investors’ money from big losses. It functioned by selling stock index futures once the prices started to tumble. In this way, the system intended to be hedged against further losses, giving the retail investors the possibility to remain in the market and at the same time to reduce their risks as low as possible.

During Black Monday, however, these insurance strategies went wrong beyond repair. As the market went down, the systems began the sell-off in large numbers, and that led to further declines and thus to the next massiveness of sales. As almost every major financial institution was using some version of the same algorithm, a feedback loop was created. The selling thus further increased itself, thereby reducing liquidity and sending tremors throughout the market. notranslate: Ususallqtsgupnlzx

“black monday 1987” proved that portfolio insurance was not a be-all end-all. The street of wealth recognized the overdependence on machines that were not overseen by people, street of wealth recognized the overdependence on machines that were not overseen by people, the street of wealth recognized the overdependence on machines without the help of humans.

Global Domino Effect and International Fallout

Most significant about Black Monday being a worldwide occurrence was the fact of the high level of interconnectedness among the markets, which was reached by the year 1987. Once the stock crashed, the world’s financial centers in London, Frankfurt, Hong Kong, and Sydney all reacted by crashing their stock exchanges. Many foreign markets experienced more precipitous drops than those in the U.S.

Some markets made a quick recovery, while others stayed down over many months or even years. The stock market crash in the USA pulled down the global economy and it showed to what extent the international markets had become intertwined.

The Federal Reserve Steps In

Fed chair Alan Greenspan spoke in the middle of the mayhem. Alan Greenspan, newly appointed chairman of the Federal Reserve, pronounced the Fed’s readiness to provide extra cash to support the financial system. The statement was indeed laconic but very forthright. The Federal Reserve, by its prompt and very firm action, aided in halting the loss and at the same time partially increased the trust of the traders.

Over the next few days, Greenspan went as far as asking banks to grant loans freely and maintain low interest rates so that the recovery can be stimulated. These actions that the Federal Reserve took are widely recognized as to prevent an extended economic descent.

Another milestone occurred when central banks across the world began to understand that their mission was not only about setting monetary policy, but also about market regulation during a financial crisis. They were the ones.

Regulatory Reforms and Circuit Breakers

An essential aspect that made Black Monday unforgettable was that it saw the birth of circuit breakers—mechanisms that stop trading automatically when prices fall too fast. These circuit breakers, also known as “cool-off” periods, are put in place to suppress irrational rather than emotional or automatic reactions from investors.

When the S&P 500 experiences a 7%, 13%, or 20% decline during a single trading day, circuit breakers come on to stop trading for different periods. Although this solution is not perfect, in general, these have become reliable systems that can be used by a country or a group of countries to avoid the panic that was on Black Monday.

The financial collapse was also a driving force behind the implementation of measures such as disclosure requirements, margin limits, and the inter-exchange coordinated system that promised the same measures for the halts and re-openings of trading in case of volatility.

A Wake-Up Call for Wall Street

The psychology aspect of Black Monday led to a change in investor’s behavior, which led to the most significant change. Namely, the rise of institutional investors who managed to put their faith in such systems, as program trading and portfolio insurance, realized that it was possible that those systems were of, instead of the assumption of risk, exacerbating the level of exposure.

It was during the event that market fragility became evident to the over-engineering of strategies. The fact was very different from the premise that contemporary finance, using models and machines, was protected from collapses.

From numerous angles, the “stock market 1987 black monday” episode had indicated a new direction. It had let the world see the numerous blunders of unmonitored innovation and paved the way for risk management protocols which were coped with till the present.

Were There Warning Signs?

The roots of Black Monday had already taken shape and been well-grown even before the disaster, as reflected by the high level of inflation, a decelerating economy, and huge trade deficits, among other causes. Currency realignment agreements, such as the Louvre Accord, had increased the level of complexity in the global markets.

That era had seen excessive valuations. It was noticeable that the price-earnings (P/E) ratio had risen above 20, a level that was usually linked to overbought conditions. However, the introduction of portfolio insurance had made the investors believe that they could take higher-than-usual risks without any negative impact.

This false sense of security along with such things as high leverage, weak fundamentals, and geopolitical uncertainty amplified the problem to the point that it was ready for a massive fire to be set on October 19, 1987.

Lessons Learnt from the 1987 Market Collapse

Whether it was the maximum point of Black Monday that is still ambiguous, what is left after the happening are the teachings.

- Liquidity is fragile: When everybody can only think of selling, and no one is ready to buy, markets will collapse.

- Automated trading requires supervision: Quite often, a good-willed algorithm may behave uncontrollably.

- Investor sentiment is extremely important: Actions of the crowd and panic have as powerful an impact as economic data.

- Regulatory changes must be implemented with the least possible delay: Credibility is the key to get through the tough times in a crisis.

The above-mentioned findings were reflected in the way both regulators and traders tackled market design in the following decades.

Have We Experienced Similar Crashes Since?

Other market catastrophes have indeed occurred after 1987; however, the speed of their occurrence is not similar. The 2001 dot-com bubble, 2008 global financial crisis, and 2020 COVID-19 crash were all characterized by sharp declines, but they occurred over days or weeks, not in minutes.

Market communication today, after the introduction of circuit breakers and better and faster, more effective technology, is certainly a more stable environment—but it is not devoid of any risk. This was recently demonstrated by the 2010 Flash Crash, when the market plunged 1,000 points in very quick succession, showing that there is still volatility in our automated systems which is just below the surface.

However, nothing has ever come close to matching the suddenness of Black Monday. It stands as a solitary point in “stock market crash history”—a kind of gauge, which is used to measure each subsequent fall in stock prices.

Is a Recurrence a Real Possibility?

Indeed, certainly. The safety nets notwithstanding, the current financial sector is more intricate, i.e., more breakable, than ever. High-speed trading, derivatives, and globalization have formed a multi-layered risk age in the interconnected world.

On the contrary, regulators are more cognizant of the situation these days. The stock market crash of 1987 is a clear example of a financial market crisis when fear outweighs logic. In the meantime, market participants are using instant information about markets and business, hands-on ways of stopping risk, and emergency data, all of which come from the very core of the crisis-experienced tools.

Even so, unanticipated events will always exist. The most visual calamities are a sudden geopolitical shock, a technological disaster, or a policy blunder. But what market players are sure of is that the “stock market 1987 black Monday” collapse will be a gruesome reminder of the consequences of irrational mass behavior.

Reflecting on the Incidents

The events of Black Monday altered our understanding of markets, technology, and human actions. Automation conflict, share-buyer hysteria, and government reaction were relevant topics almost 40 years ago but are still applicable to the present information-driven era.

The stories of the fall of the international markets to the lowest point that year are still with us to this day. Each of them i.e. breakers of the circuits, risk management systems, and real-time data are the fruits of the crisis. Nevertheless, the crash happens to be a reminder that no mechanism is flawless and one’s modesty prevails over them all.

Amid every situation of the growth of the financial market, it could be beneficial to remind all about change ability. Furthermore, history indicates that, employees’ strike groups, riots, and anything else that can be held responsible, are not there. Thus, the Madeira authorities supposed that the market would log a gain of a million reais in tourism in the future and thus kept developing the industry.

Therefore, the narration of the stock market 1987 Black Monday story is not just nostalgia, but it is a valuable reference for the future.